My Experience with Kikoff: A Real Look at Building Credit the Smart Way

Let’s talk about credit, because for a long time, it felt like this big, mysterious wall standing between me and so many things I wanted to do. Buying a car, getting a decent apartment, even just having the peace of mind that I could handle an unexpected expense – it all seemed tied to this elusive „credit score“ that I either didn’t have much of, or frankly, wasn’t doing a great job managing. Sound familiar?

I know I’m not alone in that boat. Many of us find ourselves in situations where we need to build credit from scratch, or maybe we’ve had a few bumps in the road and need to rebuild it. I was definitely in the latter category. I’d made some mistakes in my early 20s, and those lingering negative marks, combined with a thin file (meaning not a lot of active accounts reporting positive behavior), kept my score stubbornly low. Every time I checked it, I just felt frustrated. I knew I needed a change, a real strategy, something that wasn’t going to demand a perfect score to even get started.

That’s when I started looking into various credit-building tools and services. I scrolled through countless articles, read forum discussions, and watched YouTube videos. There were so many options, but a lot of them seemed to have catches: high interest rates, requiring a secured credit card with a large deposit I didn’t have readily available, or just being too complex for someone trying to get a simple foot in the door. Then, I stumbled upon Kikoff.

At first, I was skeptical, just like anyone would be with something promising a relatively easy path to credit improvement. But the more I read about Kikoff, the more it seemed to align with what I needed: a straightforward, low-cost way to establish positive payment history without a prior credit check. It felt like a breath of fresh air. I decided to take the plunge, and I’m really glad I did. This isn’t just some marketing jargon; this is my actual experience, what I saw, and how Kikoff genuinely helped me move the needle on my credit score.

If you’re curious about how Kikoff works and whether it might be the right tool for your credit journey, stick around. I’m going to walk you through my entire experience, from signing up to seeing the real-world impact. You can also Visit Official kikoff Website Now if you want to explore it for yourself right away.

What Exactly is Kikoff and How Does It Work?

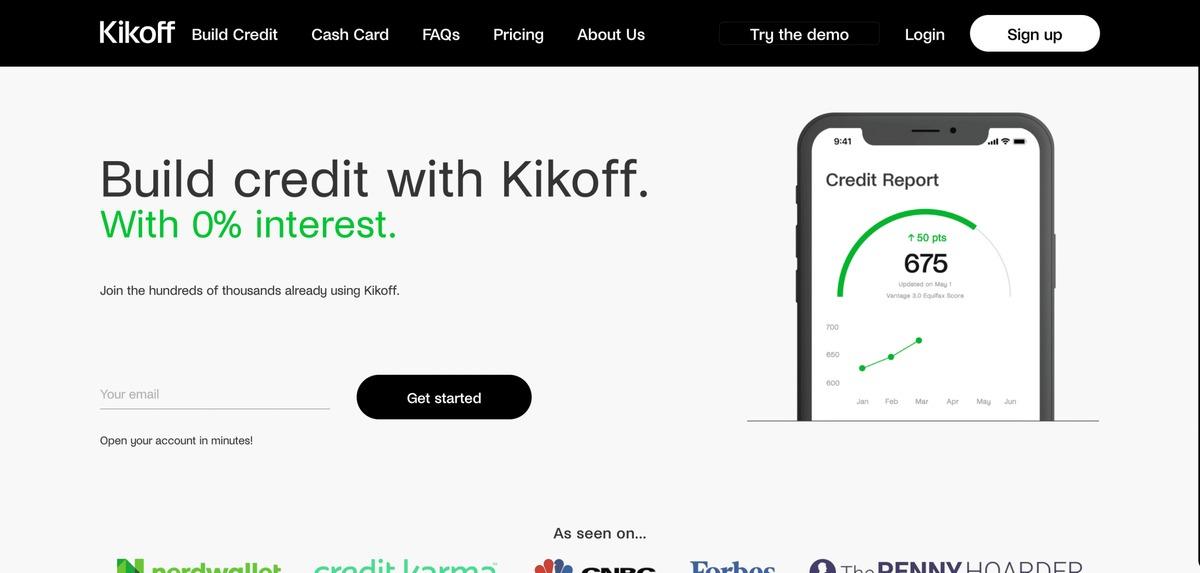

Before I dive into my personal story, let’s quickly explain what Kikoff is for those who are completely new to it. Essentially, Kikoff offers a credit builder account. It’s not a traditional loan where you get a lump sum of money, nor is it a regular credit card. Instead, it’s designed specifically to help you build a positive payment history, which is a HUGE component of your credit score.

Here’s the basic premise: When you open a Kikoff Credit Builder Account, you essentially „buy“ something small from their virtual store – think digital products like financial literacy courses or eBooks. The purchase is usually for a small amount, like $750. Instead of paying it all at once, you agree to pay it off in tiny monthly installments, typically around $5-$10. These small, consistent payments are the magic ingredient.

Kikoff then reports these on-time payments to the major credit bureaus: Equifax, Experian, and TransUnion. By consistently making these small payments, you’re demonstrating responsible financial behavior over time. This creates a positive tradeline on your credit report, showing lenders that you can manage credit and pay your bills reliably. What’s even better is that there’s no credit check to get started, which is a massive relief for anyone with a low score or no score at all. The fee for the Credit Builder Account is usually a very small monthly subscription, making it incredibly accessible.

My Personal Journey: From Skepticism to Success with Kikoff

My credit situation before Kikoff was, to put it mildly, stagnant. I had a few old collections staring me down, and the only active credit I had was my car loan, which wasn’t enough to really boost my score significantly. I knew I needed to add more positive history, but every traditional route seemed to require a credit score I just didn’t have yet. I felt stuck in a classic catch-22: „You need credit to get credit.“

Discovering Kikoff and the Sign-Up Process

I remember spending a few evenings doing deep dives online, trying to find alternative ways to build credit. Kikoff kept popping up in various recommendations. The fact that it didn’t require a credit check was a huge selling point for me. I figured, what did I have to lose? The monthly fee for the Credit Builder Account was so small, it felt like a manageable experiment.

The sign-up process itself was surprisingly smooth and quick. I went to the Kikoff website, filled out some basic personal information – name, address, Social Security Number (which they need for reporting to the credit bureaus, not for a credit check). There were no intrusive questions about my income or existing debts. It really felt like they were focused on getting me started quickly and without judgment. Within minutes, I had my account set up.

My First Kikoff Credit Builder Account: Making it Work

Once my account was active, I saw the virtual line of credit available. It wasn’t „real“ money I could spend at the grocery store, but it served its purpose perfectly for credit building. My monthly payment was set to a super affordable amount – I think it was $5 a month when I started. I immediately set up autopay from my bank account. This was crucial for me because I didn’t want to accidentally miss a payment and undo the good I was trying to do.

For the first couple of months, I didn’t see huge jumps in my credit score, and that’s important to understand. Credit building is a marathon, not a sprint. But what I did see, slowly but surely, was the Kikoff tradeline appearing on my credit reports. It was a small line of credit, but it was *there*, and it was showing consistent, on-time payments. This felt like a significant win. It was a verifiable, positive mark, something I hadn’t had much of before.

Seeing the Impact: My Credit Score Begins to Rise

After about three to four months of consistent payments, I started noticing a real difference. I use a credit monitoring service (which I highly recommend everyone does!), and I could see my score inching upwards. It wasn’t a sudden 100-point jump, but it was a steady, positive climb. My FICO score, which had been stubbornly stuck in the low 600s, started creeping into the mid-600s, and eventually even higher. This felt incredible! It wasn’t just a number; it was validation that my efforts were paying off.

What I loved about Kikoff was its simplicity. I didn’t have to think about it much after setting up autopay. It just ran in the background, quietly building my credit. It gave me a new positive account that reported good behavior, diversifying my credit mix slightly and adding to the length of my credit history over time. It truly felt like I had found an effective, low-stress way to tackle my credit goals. If you’re looking for a similar easy-to-manage solution, I strongly suggest you Visit Official kikoff Website Now.

Beyond the Credit Builder Account: The Kikoff Secured Credit Card (My Take)

Once I had established a good rhythm with my Kikoff Credit Builder Account, I started exploring their other offerings. Kikoff also has a Secured Credit Card, and this felt like the natural next step in my journey. The concept is similar to other secured cards: you make a deposit, and that deposit becomes your credit limit. What makes the Kikoff Secured Credit Card interesting is that for eligible users who have made on-time payments with their Credit Builder Account, it offers a pathway to expand your credit-building efforts without another hard pull on your credit.

I found the process of getting the secured card fairly simple, especially since I was already an existing Kikoff user. The deposit amount was flexible, allowing me to choose a limit that fit my budget. Using the secured card felt like a step up because it’s a „real“ credit card you can use for everyday purchases. This helped me practice responsible credit card usage: making small purchases I could easily pay off in full each month. This adds another type of tradeline to your report, which can be beneficial for your credit mix.

Just like with the Credit Builder Account, the key is consistency. Paying your secured card balance on time and in full every month reinforces that positive payment history. It shows lenders you can handle revolving credit responsibly. This two-pronged approach with both the Credit Builder Account and the Secured Card really accelerated my credit improvement. It provided a robust foundation for my financial future, paving the way for better interest rates and more financial flexibility down the line.

Key Benefits I Experienced with Kikoff

Looking back, here are the standout benefits that made Kikoff such a valuable tool for me:

-

Accessibility: No Credit Check to Start. This is probably the biggest game-changer for people with limited or poor credit. You’re not judged on your past, only on your commitment to build a better future. It truly levels the playing field.

-

Affordability: Low Monthly Payments. The subscription fee for the Credit Builder Account is incredibly low, usually just a few dollars a month. This makes it feasible for almost anyone to start building credit without breaking the bank.

-

Simplicity and Automation: Set It and Forget It. Once you set up autopay, Kikoff just works in the background. You don’t have to remember due dates or manage complex accounts. It’s truly a hassle-free way to build consistent payment history.

-

Real Impact on Credit Score. This isn’t just theory. I saw my credit score improve significantly over time. It gave me access to better credit products, lower interest rates, and more financial opportunities that felt out of reach before.

-

Education and Empowerment. Beyond just building credit, Kikoff also provides resources and insights into how credit works. It helped me understand the mechanics of credit scores better and empowered me to take control of my financial health.

The cumulative effect of these benefits has been profound for my financial well-being. It’s not just about a number; it’s about the doors that number opens.

Things to Consider: It’s Not a Magic Wand

While my experience with Kikoff has been overwhelmingly positive, it’s important to have realistic expectations. Kikoff is a powerful tool, but it’s not a magic wand:

-

It Takes Time: Credit building is a journey, not a sprint. You won’t see a 100-point jump overnight. Be patient and consistent, and the results will come.

-

Consistency is Key: You *must* make your payments on time. Missing a payment defeats the purpose and can actually hurt your score. Set up autopay and ensure funds are always available.

-

It’s One Piece of the Puzzle: While Kikoff provides a fantastic foundation, a truly robust credit profile usually involves a mix of credit types (revolving, installment) and a longer history. Consider adding a secured credit card or a small personal loan down the line once your Kikoff account has built up some positive history.

-

Virtual Store Limits: Remember, the initial Kikoff Credit Builder Account involves a virtual store credit, not spendable cash. Its purpose is solely for reporting payment history.

What Others Are Saying: Real Customer Feedback

My experience isn’t unique. I’ve seen countless others share similar positive stories about how Kikoff has helped them. Here’s a snapshot of what I’ve heard and read from other users:

„Before Kikoff, I couldn’t even get approved for a basic credit card. Now, after a few months, my score is up, and I feel so much more confident when applying for things. It’s truly made a difference.“ – Sarah K.

„I appreciate how straightforward Kikoff is. No hidden fees, no complex hoops to jump through, just a simple way to build payment history. The $5 a month is totally worth it for the peace of mind.“ – David L.

„I was skeptical at first, but Kikoff actually works. My credit score jumped 40 points in three months. It’s not instant, but it’s consistent progress, and that’s exactly what I needed.“ – Jessica M.

„The customer service was surprisingly helpful when I had a question about my payments. They responded quickly and professionally, which made the whole experience much smoother. Great company.“ – Robert P.

These stories resonate deeply with my own journey and highlight the consistent value Kikoff provides to people from all walks of life who are trying to improve their financial standing.

Who is Kikoff For?

Based on my experience and what I’ve learned, Kikoff is an excellent option for several groups of people:

-

Those with No Credit History: If you’re young and just starting out, or new to the country, Kikoff can help you establish your first positive tradeline.

-

Individuals Looking to Rebuild Credit: If you’ve had some financial missteps in the past, Kikoff offers a low-risk, affordable way to show new, positive payment behavior.

-

Anyone Wanting to Boost an Existing Score: Even if you have decent credit, adding another positive tradeline and diversifying your credit mix can sometimes give your score an extra lift.

-

Budget-Conscious Individuals: With its minimal monthly fee, Kikoff is accessible without requiring a large upfront investment or high annual fees.

My Final Thoughts and Recommendation

Overall, my experience with Kikoff has been incredibly positive. It delivered exactly what it promised: a simple, affordable, and effective way to build credit. It demystified the process for me and gave me a tangible tool to take control of my financial future. Seeing my credit score steadily improve wasn’t just about a number; it was about feeling more empowered, more secure, and more optimistic about my ability to achieve my financial goals.

If you’re feeling stuck with your credit, whether you’re starting from zero or trying to recover from past issues, I genuinely believe Kikoff is a fantastic resource to consider. It’s not a get-rich-quick scheme or a magical cure-all, but it is a legitimate, proven method for establishing and improving your credit health over time. The small monthly commitment is a small price to pay for the significant long-term benefits of a healthier credit score.

Don’t let credit anxiety hold you back any longer. Take the first step towards a better financial future. You can learn more and get started with your own credit-building journey today. What do you have to lose, besides those credit worries?

Ready to see how Kikoff can help you? Visit Official kikoff Website Now and explore their credit-building solutions.

Das könnte dich auch interessieren

My Deep Dive into Stacy Adams: Style, Comfort, and Everything In Between

Unser Familienurlaub am Bodensee – Pro & Contra